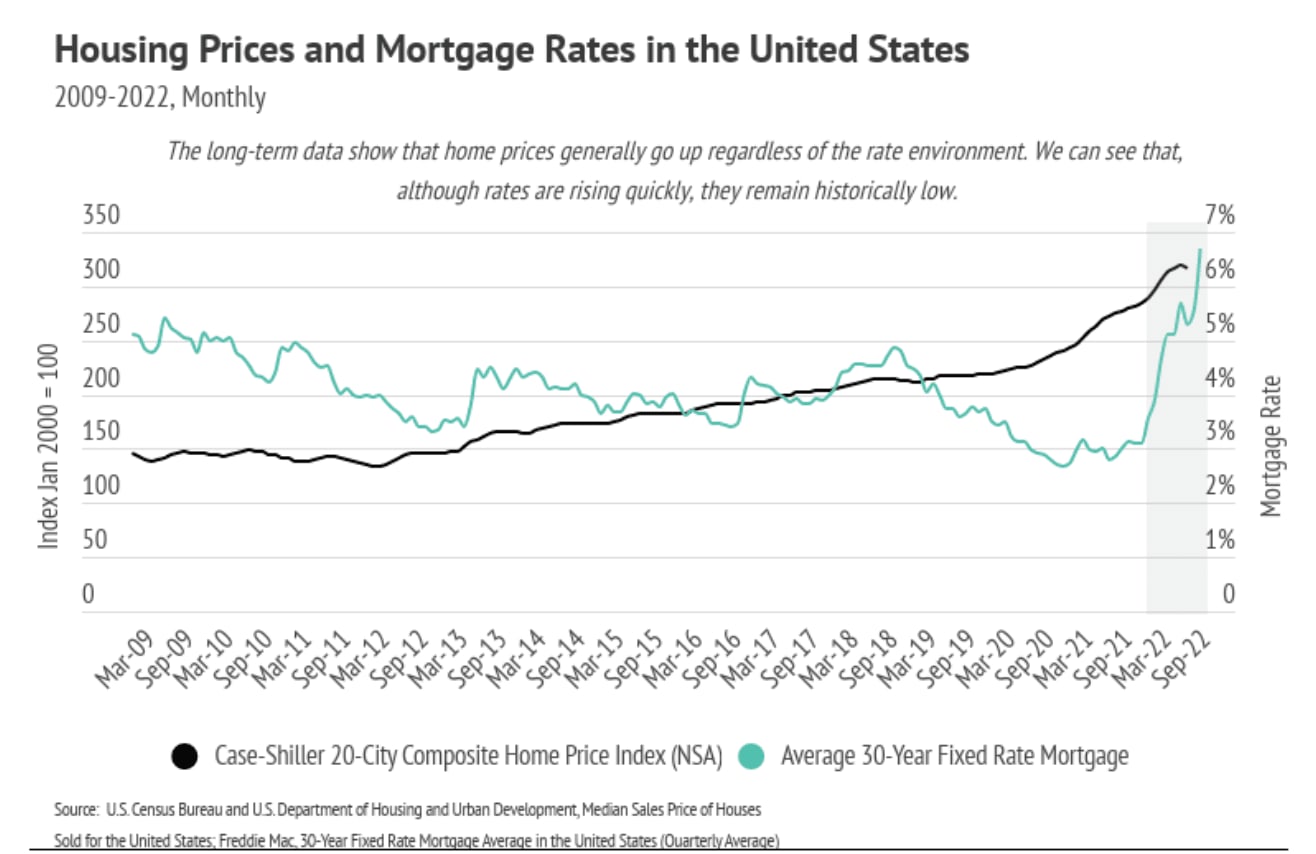

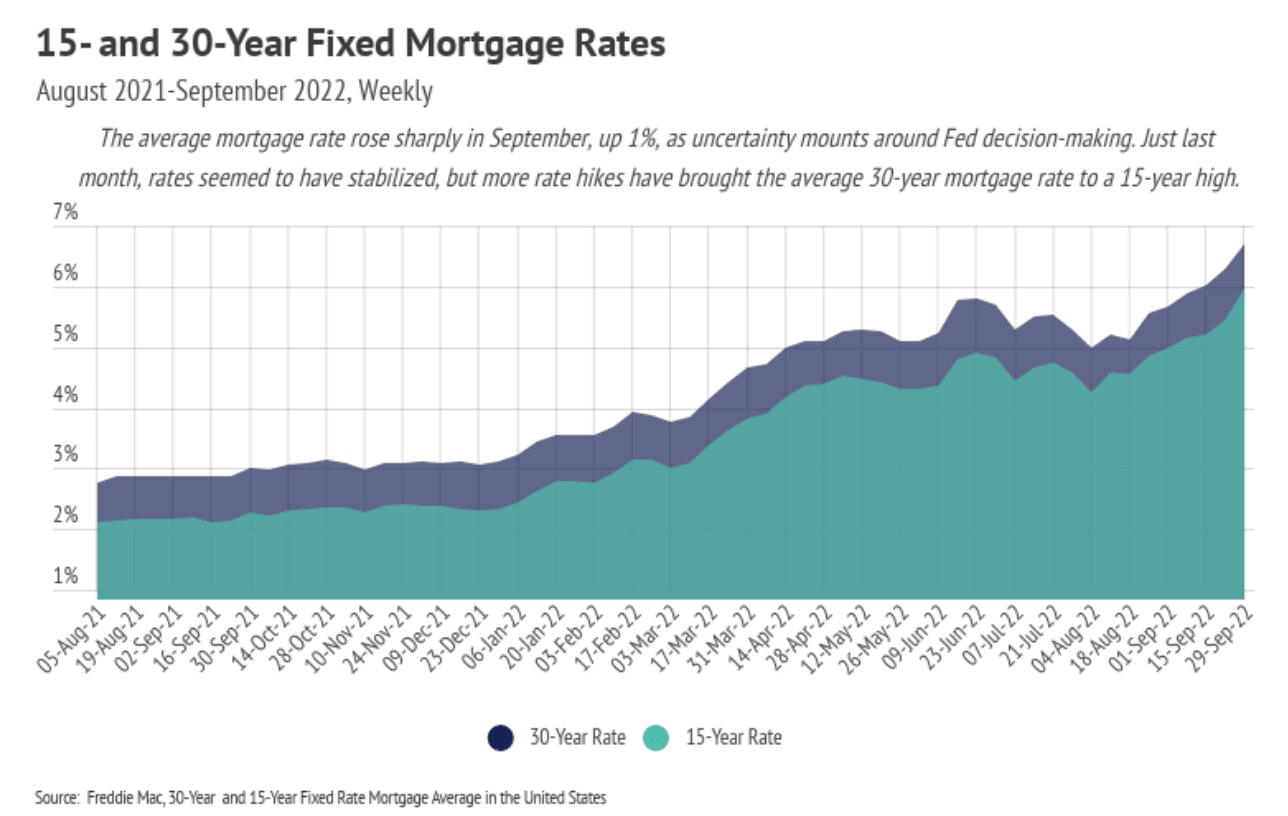

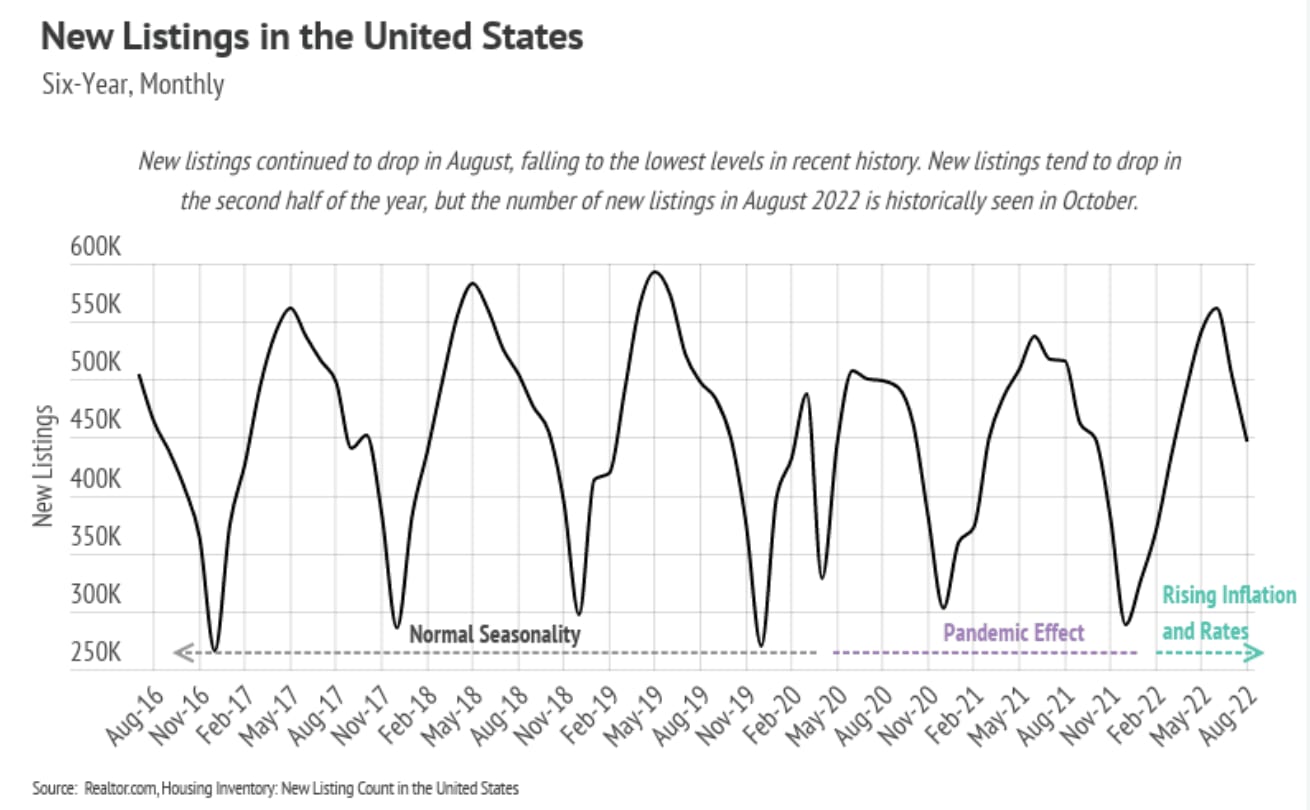

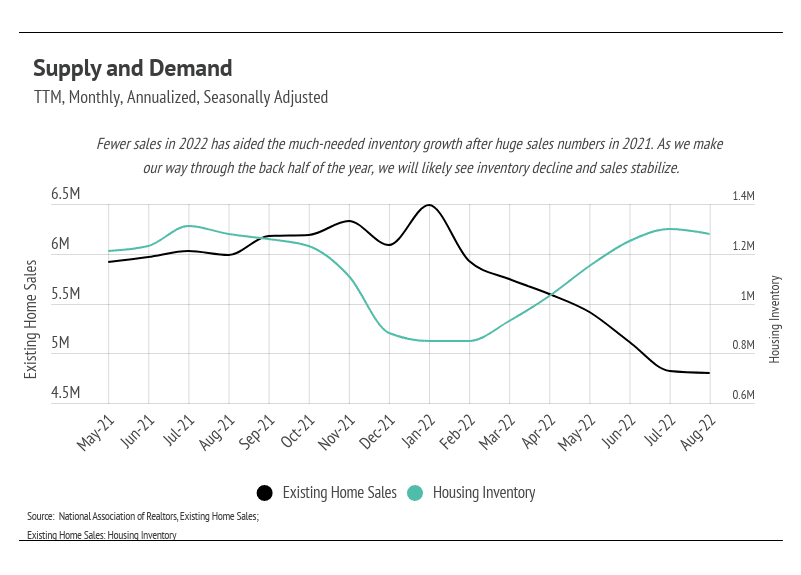

Last September, the average 30-year mortgage rate was 3.01%, meaning that a $500,000 loan would cost $2,100 per month. (That same loan now costs $3,200 per month at 6.70%.) Because the interest rate has such an outsized impact on the affordability of a home, more buyers entered the market, dropping inventory like never before. It was a great time to finance a home, and those buyers who had a down payment rightfully bought even as prices were increasing, since home prices typically continue to increase. This is actually a newer phenomenon, but one that isn’t going away. Since the mid-1990s, home prices began to move more like risk assets (stocks, bonds, commodities, etc.), which marked a huge change from the preceding 100 years. From 1890 to 1990, inflation-adjusted home prices rose only 12%, which is hard to imagine with the massive price growth, up 70% nationally, that we’ve seen over the past 10 years.